Credit Card Statements

Credit Card Statements Explained

What to look out for on your credit card statementView your credit limitThe thimbl credit card has a personalised starting credit limit between £200 and £2,000Check if you're eligible with no impact to your credit score

What to look out for on your credit card statementView your credit limitThe thimbl credit card has a personalised starting credit limit between £200 and £2,000Check if you're eligible with no impact to your credit score48.9% APR Representative (variable)

Subject to affordability

For all credit scores

For all credit scores

Check eligibility with no credit score impact

For all credit scores

Check eligibility with no credit score impact

Check eligibility with no credit score impact

For all credit scores

Check eligibility with no credit score impact

Read time: 6 minutes

Read time: 6 minutes

Published: 11th April 2025

Published: 11th April 2025

Whether you’ve just received your first, or simply want to refresh your knowledge, the thimbl guide to credit card statements shares some key information, including:

- What sort of information can be found on a credit card statement?

- How long should you keep your credit card statements?

- What should you do if you notice a transaction that you don’t recognise on your credit card statement?

What is a credit card statement?

A credit card statement is a document that contains details of your credit card transactions between a set period of time. It provides key information, such as your current balance; the minimum repayment amount that you’ll need to make; and when your next repayment is due.

How will I receive my credit card statement?

You’re likely to receive your credit card statement either in the post, via email, or through your online banking account.

You’ll be able to set your personal preference for receiving your statement in your account settings.

How often will I be sent a credit card statement?

You will usually be sent a credit card statement once a month.

If you receive your statements online, your provider may contact you by text, email, or push notification to let you know that it’s been generated and is available to view.

If the balance on your credit card account is zero, your provider might not send you a statement for that period.

When will I receive my credit card statement?

Your credit card repayment date will determine when you’ll receive your statement.

When you’re first approved for a credit card, you may be automatically set a repayment date by your provider. If you need to, you may be able to change your repayment date to suit your financial circumstances; for example, so that it falls in-line with your payday. This will then alter the date that you receive your statement.

The thimbl Credit Builder Credit Card is powered by Zable (a trading style of Lendable Limited), who aim to send out your credit card statement around 5-8 days before your payment is due.

What sort of information can I expect to find on my credit card statement?

You can expect to find the following information on your credit card statement:

- Your credit card balance. This is how much money you’ve spent on your credit card during the statement period and will include any interest.

- The minimum amount of money that you need to repay.

- Your repayment date. You’ll need to have made at least the minimum repayment by this date. You should bear in mind that depending on how you make your repayment, it may take several days for it to reach your credit card provider. To avoid the risk of being charged a late fee, you should ensure that your repayment is made in plenty of time before the date it’s due.

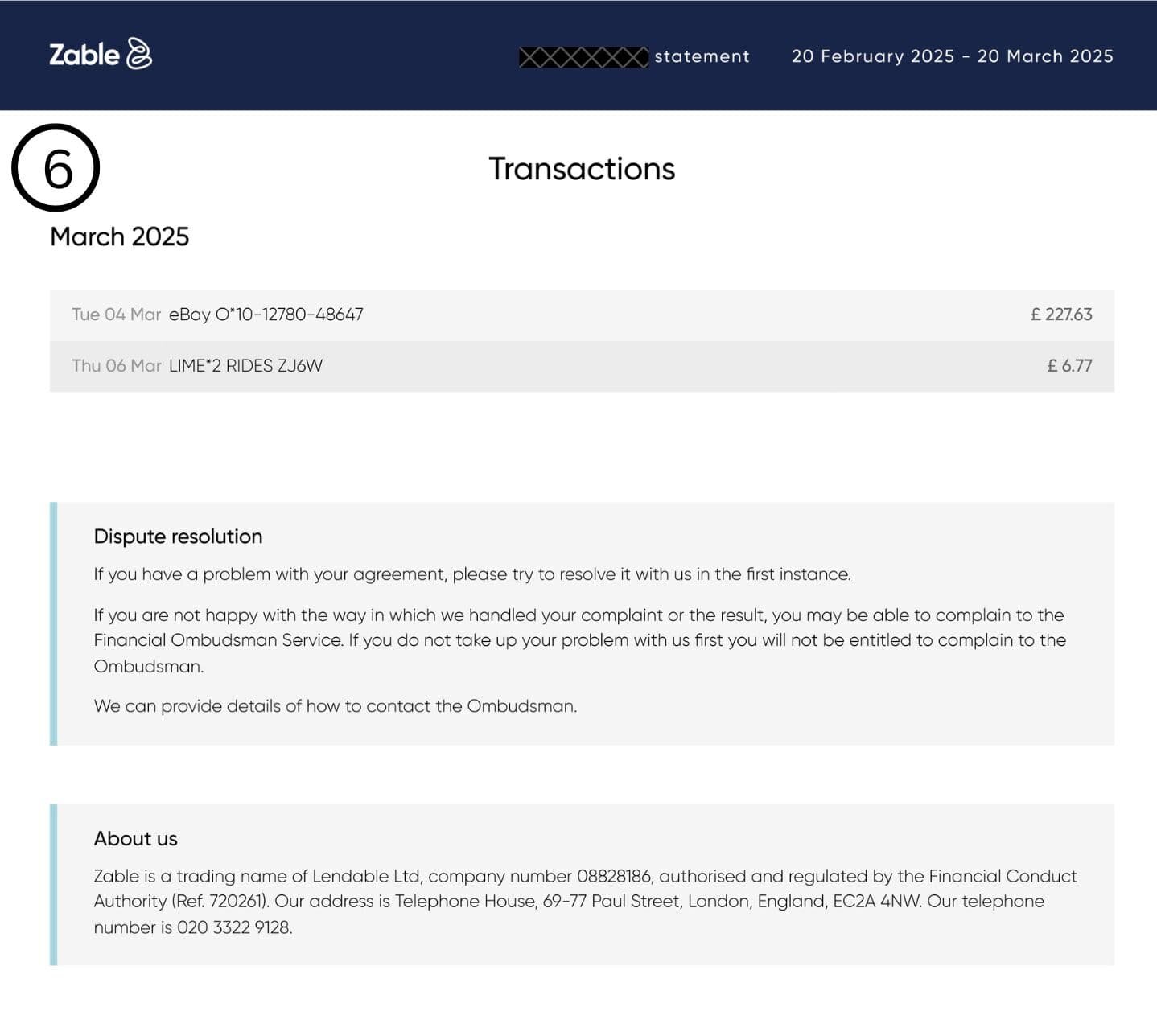

- A summary of the transactions made since your last statement or, if it’s your first statement, the transactions made since your account was opened. This will include how much money you’ve spent and where the transaction was made.

- ny applicable fees that you might have been charged.

- Some basic details, such as your credit card number; total credit limit; and your monthly and annual interest rate.

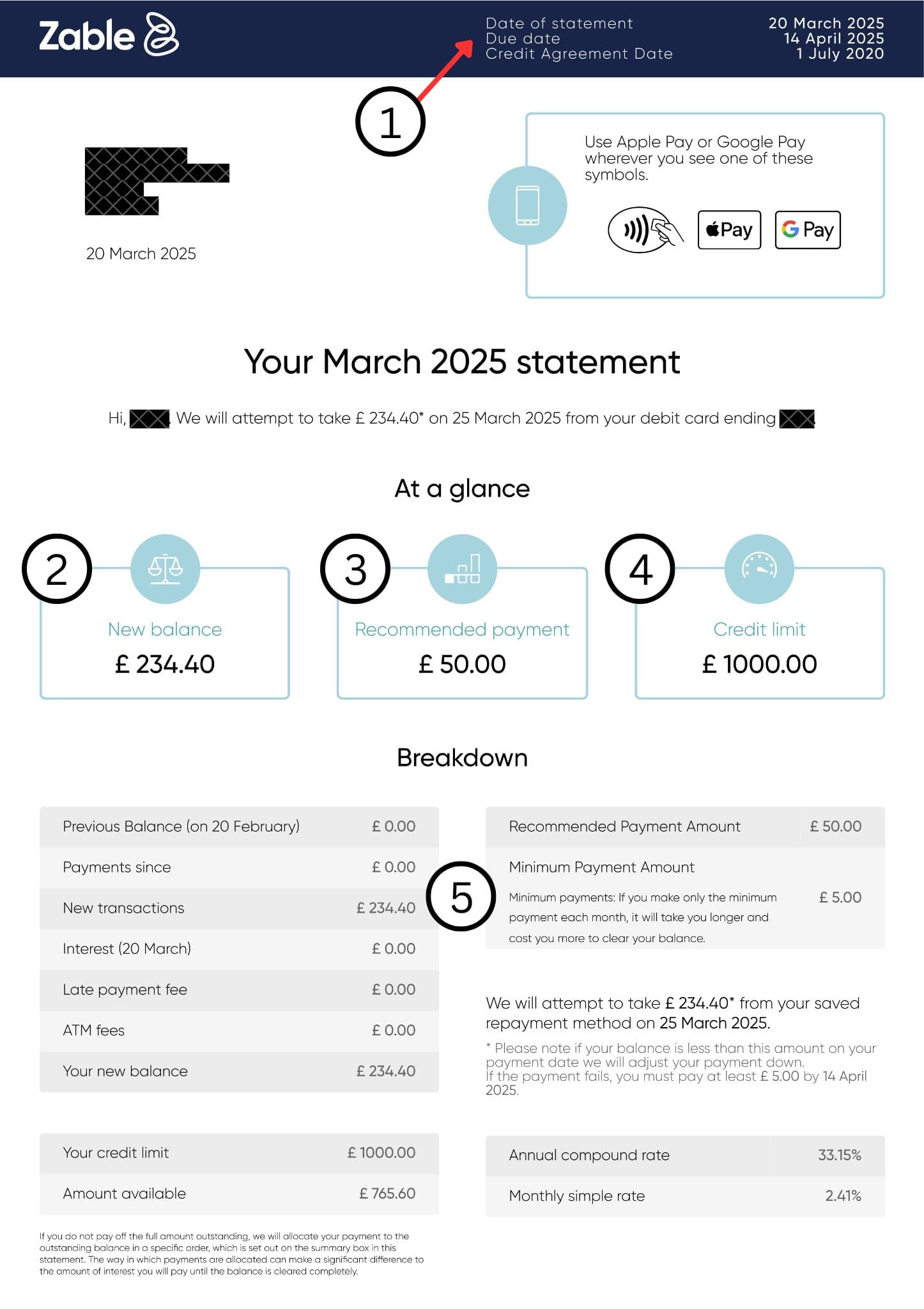

We’ve included an example statement from our credit card partner, Zable.

- Due date: this is the date by which you’ll need to make at least the minimum repayment.

- New balance: the overall amount of money you’ve spent on your credit card.

- Recommended payment: The recommended repayment amount is 6% of your balance.

- Credit limit: the total amount of money that you can spend on your credit card. Remember, you should never spend more money than you need to or can afford to repay.

- Minimum repayment amount: the minimum amount you’ll need to pay off your balance.

- Transaction history: a summary of your spending and repayment activity during the billing cycle. You should check this carefully to make sure that you recognise each transaction listed.

How soon after receiving my statement should I repay my credit card?

Your credit card statement will tell you the date by which you’ll need to make your repayment, but you can choose to make your repayment before this if you’d like to.

How can I repay my credit card?

You can choose to repay your credit card by Direct Debit, standing order, or by bank transfer. You’ll be able to find more details on the back of your credit card statement.

When you make a repayment, you can either:

- Pay the minimum amount;

- Pay more than the minimum amount; or

- Clear the balance in full.

Can I pay more than the minimum repayment amount?

Yes, you can. As long as you meet the minimum repayment amount, you can pay as much of your balance as you like.

If you clear your balance in full and on time each month, you won’t be charged interest.

What should I do if I spot an unrecognised transaction on my credit card statement?

The first thing you should do in this situation is take some time to try and identify the transaction.

- Do some research. Some retailers may operate under a different trading name, which can sometimes cause confusion.

- Check the date of the payment and any other transactions that were made around a similar time. This could help jog your memory of a transaction that you might have forgotten about.

- Do you have a joint account? If so, could the person you share the account with have made the payment?

- Have you signed up for any free trials, such as a subscription service or a gym? Perhaps you’ve forgotten to cancel your free trial and have been charged – easily done!

- Have you made a booking; for example, a hotel stay or restaurant reservation, that required a pre-authorisation payment?

If you’re still unsure about the transaction, you should contact your provider as soon as possible.

How long do I have to dispute about something on my credit card statement?

Every provider is different, but generally, you’ll have around 60 days to raise a dispute about an unrecognised transaction on your credit card statement. You may wish to contact your provider sooner, rather than later, so that they can investigate the issue.

Should I keep my old credit card statements?

You should keep hold of any paper-copy credit card statements for at least 60 days. Digital statements will typically be retained in your online account, but you may wish to download a copy and store it on your device for future reference.

Will I get an annual credit card statement?

It’s likely that you’ll be sent a credit card statement with a summary of your annual transactions. Your first annual statement will typically be sent approximately 12 months after you first opened your account.

What happens if I can’t afford to repay my credit card?

Making a late repayment or missing one altogether could result in late fees and charges, financial stress, and a decline to your credit score.

If you’re struggling to make your credit card repayments, you should contact your provider. There may be things they can suggest to help you through this challenging time.

If you need help with your finances…

Many of us will experience money worries at some point in our lives. Financial difficulties are nothing to be ashamed of.

Please know that you can access free, confidential advice on money and debt management through charities and organisations such as StepChange, MoneyHelper, Citizens Advice, and National Debtline.

Page last reviewed: 11th February 2025

Page reviewed by: Alex Kosuth-Phillips

You get all this with thimbl

Tap and go

Quick and easy contactless payments up to £100.

Secure banking app

Manage your credit card online, wherever and whenever you like, with the free mobile app.

A trusted service

Over 4,500 positive reviews from our customers.

48.9% APR Representative (variable)

Quick links

Worried about money?

If you're worried about the cost of living, need support with budgeting, or think you might need debt advice, StepChange could help. They offer free and impartial support and help hundreds of thousands of people every year to deal with their debts and take control of their finances.

To find out how StepChange could help you, take the free Money Health Check. It's quick and easy to complete, and will give you a personalised recommendation on what to do next.

Credit Builder Credit Card

Over 150,000 people have already been accepted for a thimbl Credit Builder Credit Card

Check if you're eligible with no impact to your credit scorePersonalised credit limit between £200 and £2,000

Check if you're eligible with no impact to your credit scorePersonalised credit limit between £200 and £2,00048.9% APR Representative (variable)

Meet the team

Head of Compliance

Head of Partnerships

Managing Director, thimbl

Marketing Manager

Financial Content Writer

Frequently asked

questions

If you've got a question, you may just find the answer you're looking for here. If not, please visit our contact us page and get in touch.

What is thimbl?

Can I apply for a credit card with no credit score?

Can I apply for a credit card without a credit check?

What’s the difference between no credit history and bad credit history?

Bad credit history could be a result of several factors, including past poor financial management such as missed payments and bankruptcy, using a credit card to withdraw money from a cash machine, and even being the victim of fraud. Both a thin credit file and bad credit history could make applying for credit challenging.

A credit builder credit card could be a suitable option for people hoping to establish their credit score or move towards a healthier credit position.

Did you find this article helpful?

Let us know how we can be more helpful

Please leave your anonymous feedback to help us keep improving.

Need help or support?

Whether it’s a question or you just need support, we’re here to help.